For this year’s Automobile Symposium Wildau, our colleagues Klaus Schöpflin, Lukas Zühlke and Christina Schöpflin have brought their contribution on the topic of digitalisation and payment solutions in the automobile industry. Their article entitled Payment solutions for digital business models in the automobile industry has also been published in the AKWI-Journal for applications and concepts in business informatics.

In the next weeks we shall gradually publish the article on our website as well.

PAYMENT SOLUTIONS FOR DIGITAL BUSINESS MODELS IN THE AUTOMOBILE INDUSTRY – OBSERVATIONS FROM THE USERS’ POINT OF VIEW

BY KLAUS SCHÖPFLIN, LUKAS ZÜHLKE, CHRISTINA SCHÖPFLIN

Compared to typical offers from the online or mobile commerce, there are few multi-channel compatible offers and services in the automobile industry. Furthermore, those offers and services show explicit weaknesses in the handling of registration- and payment processes compared to other branches.

On the other hand, automobile manufacturers have already invested a lot of money and effort in the development of proprietary payment methods – without visible success. Additionally, there are far more technical possibilities available that are not yet used. Why?

Looking at the available payment solutions offered by automobile manufacturers on the market for the previously mentioned applications, clear weaknesses regarding the “usability” of these uses can generally be derived, in particular:

- Circuitous registration processes

- No consistent interface

- Many media discontinuities

- No consistent or missing non-cash payment methods

- Simple “additional order” often not possible

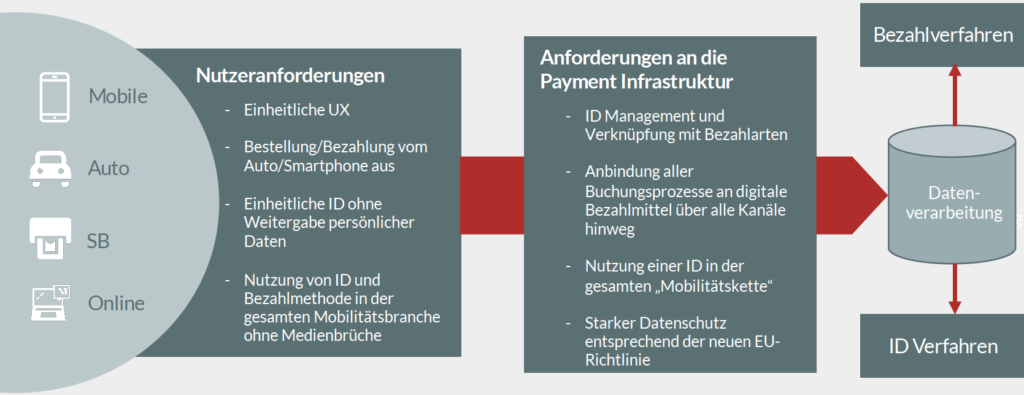

Typical user requirements can easily be derived from comparable applications in other fields, such as online trade. This concerns not only the “user experience” regarding the execution of payment processes, but also

- Consistent user interfaces for all “touch points” (mobile, online, vending machines, car)

- Immediately usable multi-channel offers

- The usage of consistent identification characteristics

- Protective mechanisms for personal data.

Both these fundamental user requirements and the experiences made with digital payment solutions in other fields give important insights for the basic architecture of payment solutions.

Payment is a means to an end. The focus must lay on the “consumption” of digital services. Nobody likes to pay.

Therefore, for a payment infrastructure to be attractive to users, it needs to include the following characteristics:

- ID-Management and connections with payment types and functions

- Connection of all booking, ordering and payment processes to multi-channel compatible payment means

- Usage of one ID for the entire “mobility environment”

- Strong data privacy according to the new EU-guidelines

Figure 2: Typical user requirements and requirements to the payment-infrastructure

The technical implementation of such an architecture is already possible, since the basic partial applications have already been introduced to the market. When purchasing and integrating such partial applications, the strategic question of “build, buy or partner” comes up for important fundamental solutions (e.g. payment gateway).

The decisive success factor though is less the IT-architecture, as the business architecture of a highly scalable payment solution. Finding „successful role models in the payment industry and understanding the predominant market conditions and success factors are of significant importance.